/ May 30, 2025

Trending

Homeowners who purchased in the last year or so could drive themselves nuts trying to find the perfect time to refinance. After all, it hurt bad enough to miss out on those once-in-a-lifetime low rates of 2020 and 2021, and it’s hard to pull the trigger when refinancing today could potentially mean missing out on even lower rates next week.

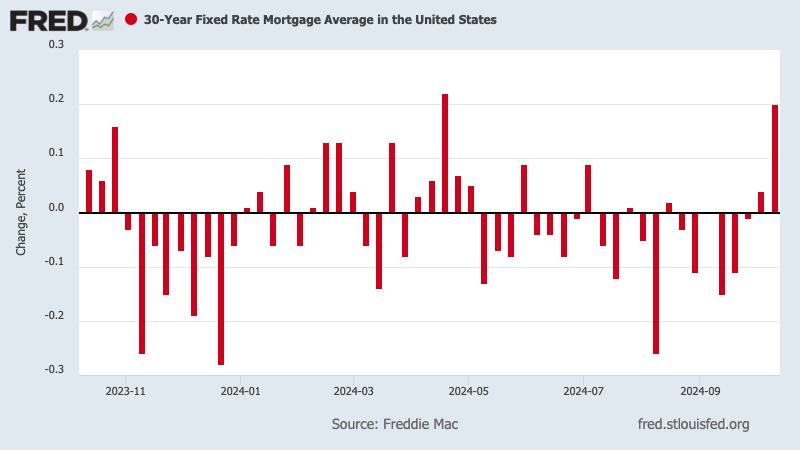

This week was a great example of how much mortgage interest rates can change in a short window of time. The 30-year fixed-rate mortgage rate spiked 21 basis points to an average of 6.4%. That’s a whopping 51 basis points more than in the week ending Sept. 19, immediately following the last Federal Reserve meeting. A basis point is one one-hundredth of a percentage point.

Rather than waiting for rates to hit their lowest, homeowners may be better off calculating what rate would give them a reasonable break-even point — the number of months or years it would take to recoup the refinancing costs — and make that their goal.

For instance, suppose a borrower got a $300,000 30-year conventional mortgage in early October 2023 at a rate of 7.5%, which was typical for that time. Refinancing to 6.12% — the average rate posted by Freddie Mac on Oct. 3, 2024 — would result in monthly savings of nearly $300 and savings of $80,155 over the entire life of the loan. Assuming the borrower pays $6,500 in closing costs, the break-even point would be 22 months, or just under two years.

While Fed watchers are predicting further cuts to the federal funds rate through the rest of this year, mortgage rates don’t have to vary much to create sizable implications for the refi market. According to an October report from real estate tech firm ICE Mortgage Technology, rates falling from 6.4% in August to 6.1% in September grew the number of households who would benefit from refinancing by 1.3 million. An additional mortgage rate drop of 25 basis points (which is within a fair range of normal weekly or even daily changes) would add another 1.2 million to that pool of potential refi candidates.

On the flip side, an Oct. 9 Zillow analysis of homebuying data estimates that approximately 275,000 more households would benefit by refinancing at 6.1% than at 6.6%. According to Zillow, that 0.5-percentage-point rate increase represents a combined loss of over $6 billion in potential refinance savings over five years.

If you find that refinancing may soon be on the table after you’ve calculated your target rate, you can prepare by getting your financial profile in shape.

utm_campaign=ct_prod&utm_content=1643704&utm_medium=rss&utm_source=syndication&utm_term=medianews-group” target=”_self” rel=”nofollow noopener”>Get a copy of your credit report

, and contact the credit reporting bureaus if you note any mistakes. Pay down existing debts as much as possible, as lowering your debt-to-income ratio will make you a more attractive borrower and can get you a lower interest rate. You should also avoid making any large purchases on credit, like buying a new car or financing new furniture.

Additionally, if you’ve only recently purchased your home, review your closing contract to see if there’s a prepayment penalty for refinancing before a certain number of months have passed. If you’re stuck with that fee, you’ll want to factor that into your break-even calculations and see if that affects your goal rate.

Originally Published:

Homeowners who purchased in the last year or so could drive themselves nuts trying to find the perfect time to refinance. After all, it hurt bad enough to miss out on those once-in-a-lifetime low rates of 2020 and 2021, and it’s hard to pull the trigger when refinancing today could potentially mean missing out on even lower rates next week.

This week was a great example of how much mortgage interest rates can change in a short window of time. The 30-year fixed-rate mortgage rate spiked 21 basis points to an average of 6.4%. That’s a whopping 51 basis points more than in the week ending Sept. 19, immediately following the last Federal Reserve meeting. A basis point is one one-hundredth of a percentage point.

Rather than waiting for rates to hit their lowest, homeowners may be better off calculating what rate would give them a reasonable break-even point — the number of months or years it would take to recoup the refinancing costs — and make that their goal.

For instance, suppose a borrower got a $300,000 30-year conventional mortgage in early October 2023 at a rate of 7.5%, which was typical for that time. Refinancing to 6.12% — the average rate posted by Freddie Mac on Oct. 3, 2024 — would result in monthly savings of nearly $300 and savings of $80,155 over the entire life of the loan. Assuming the borrower pays $6,500 in closing costs, the break-even point would be 22 months, or just under two years.

While Fed watchers are predicting further cuts to the federal funds rate through the rest of this year, mortgage rates don’t have to vary much to create sizable implications for the refi market. According to an October report from real estate tech firm ICE Mortgage Technology, rates falling from 6.4% in August to 6.1% in September grew the number of households who would benefit from refinancing by 1.3 million. An additional mortgage rate drop of 25 basis points (which is within a fair range of normal weekly or even daily changes) would add another 1.2 million to that pool of potential refi candidates.

On the flip side, an Oct. 9 Zillow analysis of homebuying data estimates that approximately 275,000 more households would benefit by refinancing at 6.1% than at 6.6%. According to Zillow, that 0.5-percentage-point rate increase represents a combined loss of over $6 billion in potential refinance savings over five years.

If you find that refinancing may soon be on the table after you’ve calculated your target rate, you can prepare by getting your financial profile in shape.

utm_campaign=ct_prod&utm_content=1643704&utm_medium=rss&utm_source=syndication&utm_term=medianews-group” target=”_self” rel=”nofollow noopener”>Get a copy of your credit report

, and contact the credit reporting bureaus if you note any mistakes. Pay down existing debts as much as possible, as lowering your debt-to-income ratio will make you a more attractive borrower and can get you a lower interest rate. You should also avoid making any large purchases on credit, like buying a new car or financing new furniture.

Additionally, if you’ve only recently purchased your home, review your closing contract to see if there’s a prepayment penalty for refinancing before a certain number of months have passed. If you’re stuck with that fee, you’ll want to factor that into your break-even calculations and see if that affects your goal rate.

Originally Published: